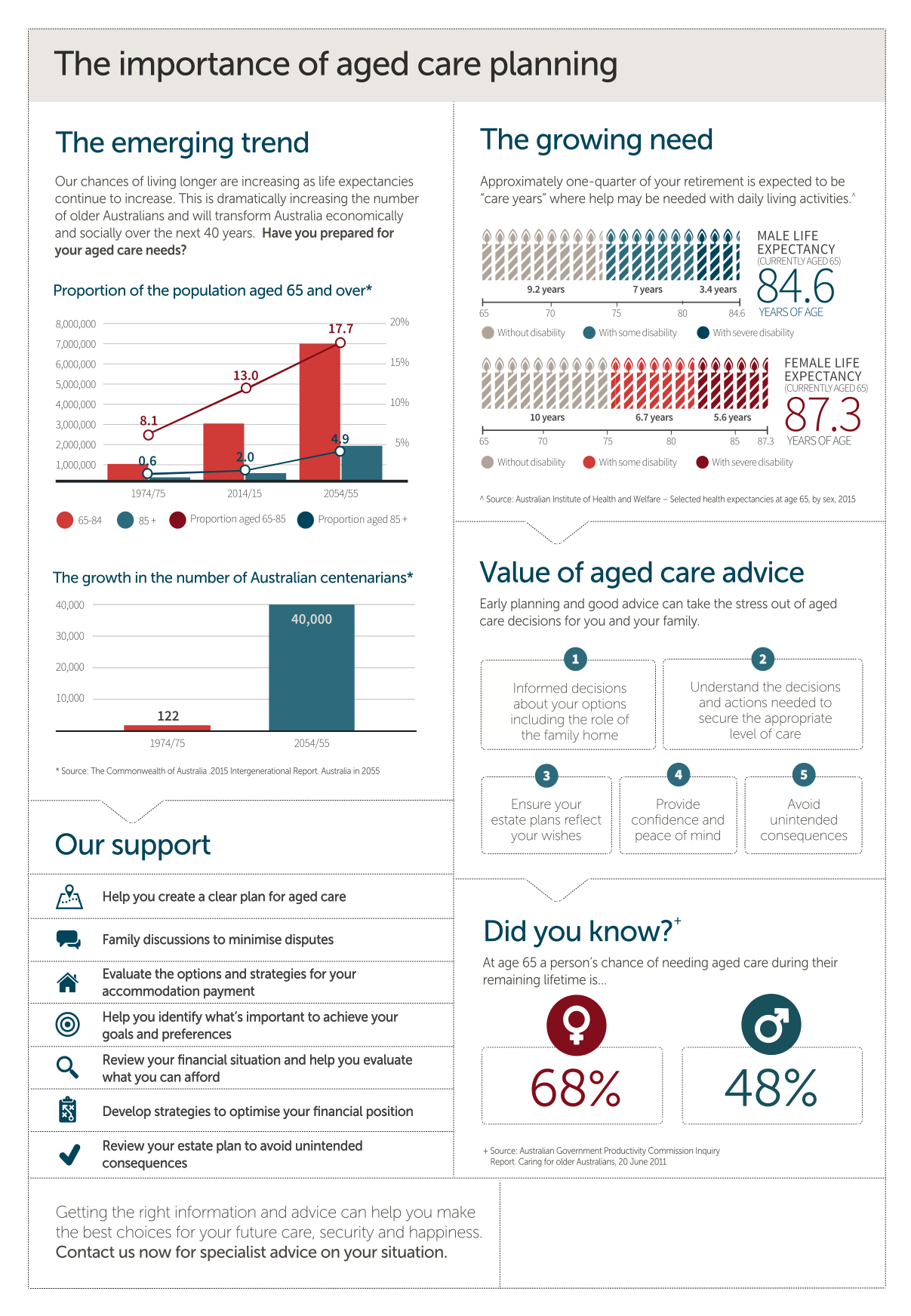

Last year we all had a taste of what it is like to lose some independence and be confined at home. Not able to get out. And not easy to see the doctor or do the groceries without some planning ahead.

But what if the reason was not an international pandemic and was not affecting everyone in your street, just you? What if it was due to your own frailty?

With the potential for frailty (on average) to span 20% of our retirement years, we need a plan. We need to think ahead. Decide what is important. Identify the trigger points. Socialise the plan with our family.

While this may sound grim, it is not all bad. Having a plan can set you up to have choices and more control so you can maintain as much independence as possible. If frailty creeps up and you have not planned ahead, you might find yourself herded down a path based on the bias and the goals (no matter how well-intentioned) of the person who first says “I can help”.

A plan gives you time to consider your preferred choices and be prepared. This may allow you to:

- Ensure your home is modified and ready to continue living there.

- Have your support teams in place.

- Take away some of the stress and uncertainty from your family.

- And most importantly, have the finances ready to pay for the support you need to ensure not only quality of care, but also the quality of lifestyle.

But not everything always goes our way or how we planned. This is why planning is important. You can add contingency measures and decision pathways into your plan. So how do you get started?

Don’t do it alone. It is too hard to be objective. Seek out the experts. Ask your financial planner for help. This is what we are good at … planning.

In our business we believe in helping clients throughout retirement and continually review and modify plans so that the changes needed at life’s transition points can be implemented smoothly and effectively. We can also help with your family discussions. We have advisers who are Accredited Aged Care Professionals TM who are ready to help.

Contact us today to make an appointment to discuss your current or future aged care needs.

Please contact Integrity One if we can assist you with this or any other financial matter.

Phone: (03) 9723 0522

Suite 2, 1 Railway Crescent

Croydon, Victoria 3136

Email: integrityone@iplan.com.au

This information is of a general nature and does not take into consideration anyone’s individual circumstances or objectives. Financial Planning activities only are provided by Integrity One Planning Services Pty Ltd as a Corporate Authorised Representative No. 315000 of Integrity Financial Planners Pty Ltd ABN 71 069 537 855 AFSL 225051. Integrity One Planning Services Pty Ltd and Integrity One Accounting and Business Advisory Services Pty Ltd are not liable for any financial loss resulting from decisions made based on this information. Please consult your adviser, finance specialist, broker, and/or accountant before making decisions using this information.